Note

This page was generated from docs/tutorials/08_cvar_optimization.ipynb.

Improving Variational Quantum Optimization using CVaR¶

Introduction¶

This notebook shows how to use the Conditional Value at Risk (CVaR) objective function introduced in [1] within the variational quantum optimization algorithms provided by Qiskit Algorithms. Particularly, it is shown how to setup the MinimumEigenOptimizer using SamplingVQE accordingly. For a given set of shots with corresponding objective values of the considered optimization problem, the CVaR with confidence level

\(\alpha \in [0, 1]\) is defined as the average of the \(\alpha\) best shots. Thus, \(\alpha = 1\) corresponds to the standard expected value, while \(\alpha=0\) corresponds to the minimum of the given shots, and \(\alpha \in (0, 1)\) is a tradeoff between focusing on better shots, but still applying some averaging to smoothen the optimization landscape.

References¶

[1] P. Barkoutsos et al., Improving Variational Quantum Optimization using CVaR, Quantum 4, 256 (2020).

[1]:

import matplotlib.pyplot as plt

import numpy as np

from docplex.mp.model import Model

from qiskit.circuit.library import real_amplitudes

from qiskit.primitives import StatevectorSampler

from qiskit_optimization.algorithms import MinimumEigenOptimizer

from qiskit_optimization.converters import LinearEqualityToPenalty

from qiskit_optimization.minimum_eigensolvers import NumPyMinimumEigensolver, SamplingVQE

from qiskit_optimization.optimizers import COBYLA

from qiskit_optimization.translators import from_docplex_mp

from qiskit_optimization.utils import algorithm_globals

/tmp/ipykernel_16022/311796302.py:4: DeprecationWarning: Using Qiskit with Python 3.9 is deprecated as of the 2.1.0 release. Support for running Qiskit with Python 3.9 will be removed in the 2.3.0 release, which coincides with when Python 3.9 goes end of life.

from qiskit.circuit.library import real_amplitudes

[2]:

algorithm_globals.random_seed = 123456

Portfolio Optimization¶

In the following we define a problem instance for portfolio optimization as introduced in [1].

[3]:

# prepare problem instance

n = 6 # number of assets

q = 0.5 # risk factor

budget = n // 2 # budget

penalty = 2 * n # scaling of penalty term

[4]:

# instance from [1]

mu = np.array([0.7313, 0.9893, 0.2725, 0.8750, 0.7667, 0.3622])

sigma = np.array(

[

[0.7312, -0.6233, 0.4689, -0.5452, -0.0082, -0.3809],

[-0.6233, 2.4732, -0.7538, 2.4659, -0.0733, 0.8945],

[0.4689, -0.7538, 1.1543, -1.4095, 0.0007, -0.4301],

[-0.5452, 2.4659, -1.4095, 3.5067, 0.2012, 1.0922],

[-0.0082, -0.0733, 0.0007, 0.2012, 0.6231, 0.1509],

[-0.3809, 0.8945, -0.4301, 1.0922, 0.1509, 0.8992],

]

)

# or create random instance

# mu, sigma = portfolio.random_model(n, seed=123) # expected returns and covariance matrix

[5]:

# create docplex model

mdl = Model("portfolio_optimization")

x = mdl.binary_var_list(range(n), name="x")

objective = mdl.sum([mu[i] * x[i] for i in range(n)])

objective -= q * mdl.sum([sigma[i, j] * x[i] * x[j] for i in range(n) for j in range(n)])

mdl.maximize(objective)

mdl.add_constraint(mdl.sum(x[i] for i in range(n)) == budget)

# case to

qp = from_docplex_mp(mdl)

[6]:

# solve classically as reference

opt_result = MinimumEigenOptimizer(NumPyMinimumEigensolver()).solve(qp)

print(opt_result.prettyprint())

objective function value: 1.27835

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

[7]:

# we convert the problem to an unconstrained problem for further analysis,

# otherwise this would not be necessary as the MinimumEigenSolver would do this

# translation automatically

linear2penalty = LinearEqualityToPenalty(penalty=penalty)

qp = linear2penalty.convert(qp)

_, offset = qp.to_ising()

Minimum Eigen Optimizer using SamplingVQE¶

[8]:

# set classical optimizer

maxiter = 100

optimizer = COBYLA(maxiter=maxiter)

# set variational ansatz

ansatz = real_amplitudes(n, reps=1)

m = ansatz.num_parameters

# set sampler

sampler = StatevectorSampler(seed=123, default_shots=1000)

# run variational optimization for different values of alpha

alphas = [1.0, 0.50, 0.25] # confidence levels to be evaluated

[9]:

# dictionaries to store optimization progress and results

objectives = {alpha: [] for alpha in alphas} # set of tested objective functions w.r.t. alpha

results = {} # results of minimum eigensolver w.r.t alpha

# callback to store intermediate results

def callback(i, params, obj, stddev, alpha):

# we translate the objective from the internal Ising representation

# to the original optimization problem

objectives[alpha].append(np.real_if_close(-(obj + offset)))

# loop over all given alpha values

for alpha in alphas:

# initialize SamplingVQE using CVaR

vqe = SamplingVQE(

sampler=sampler,

ansatz=ansatz,

optimizer=optimizer,

aggregation=alpha,

callback=lambda i, params, obj, stddev: callback(i, params, obj, stddev, alpha),

)

# initialize optimization algorithm based on CVaR-SamplingVQE

opt_alg = MinimumEigenOptimizer(vqe)

# solve problem

results[alpha] = opt_alg.solve(qp)

# print results

print("alpha = {}:".format(alpha))

print(results[alpha].prettyprint())

print()

alpha = 1.0:

objective function value: 0.7296000000000049

variable values: x_0=0.0, x_1=1.0, x_2=1.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

alpha = 0.5:

objective function value: 1.2783500000000174

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

alpha = 0.25:

objective function value: 1.2783500000000174

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

[10]:

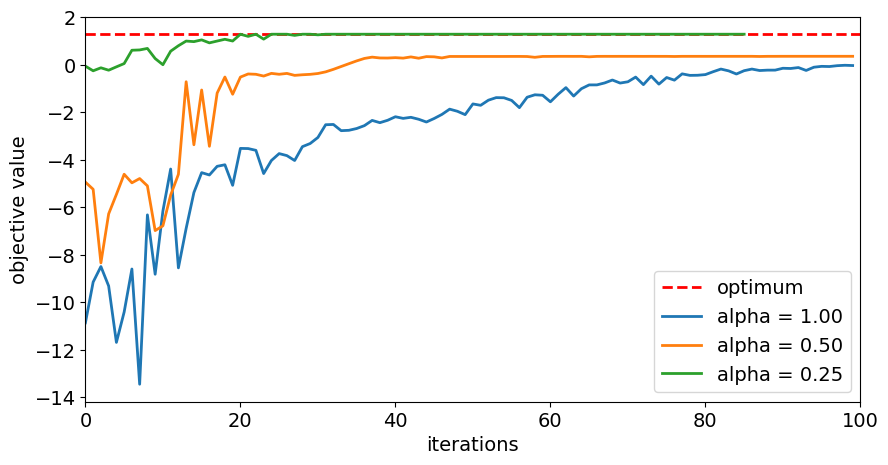

# plot resulting history of objective values

plt.figure(figsize=(10, 5))

plt.plot([0, maxiter], [opt_result.fval, opt_result.fval], "r--", linewidth=2, label="optimum")

for alpha in alphas:

plt.plot(objectives[alpha], label="alpha = %.2f" % alpha, linewidth=2)

plt.legend(loc="lower right", fontsize=14)

plt.xlim(0, maxiter)

plt.xticks(fontsize=14)

plt.xlabel("iterations", fontsize=14)

plt.yticks(fontsize=14)

plt.ylabel("objective value", fontsize=14)

plt.show()

[11]:

# evaluate and sort all objective values

objective_values = np.zeros(2**n)

for i in range(2**n):

x_bin = ("{0:0%sb}" % n).format(i)

x = [0 if x_ == "0" else 1 for x_ in reversed(x_bin)]

objective_values[i] = qp.objective.evaluate(x)

ind = np.argmax(objective_values)

# evaluate final optimal probability for each alpha

for alpha in alphas:

probabilities = np.zeros(2**n)

prob_dict = results[alpha].min_eigen_solver_result.eigenstate.binary_probabilities()

for key, val in prob_dict.items():

probabilities[int(key, 2)] = val

print("optimal probability (alpha = %.2f): %.4f" % (alpha, probabilities[ind]))

optimal probability (alpha = 1.00): 0.0000

optimal probability (alpha = 0.50): 0.0050

optimal probability (alpha = 0.25): 0.3010

[12]:

import tutorial_magics

%qiskit_version_table

%qiskit_copyright

Version Information

| Software | Version |

|---|---|

qiskit | 2.1.2 |

qiskit_optimization | 0.7.0 |

| System information | |

| Python version | 3.9.23 |

| OS | Linux |

| Wed Aug 20 14:17:30 2025 UTC | |

This code is a part of a Qiskit project

© Copyright IBM 2017, 2025.

This code is licensed under the Apache License, Version 2.0. You may

obtain a copy of this license in the LICENSE.txt file in the root directory

of this source tree or at http://www.apache.org/licenses/LICENSE-2.0.

Any modifications or derivative works of this code must retain this

copyright notice, and modified files need to carry a notice indicating

that they have been altered from the originals.

[ ]: